已投注了或表演继续

FRS have used the moment of a surge in market optimism for an increase in a rate. Large players reacted not only with the sale of the dollar, but also active demand for risk assets. Now market prospects of dollar depend only on Trump's administration and the Congress of the USA.

The FRS decision caused ambiguous movements in the markets: the dollar not only didn't become stronger, it simply failed, and treasures profitability goes down too. Apparently, expectations of the market participants were overestimated: they were afraid of the Federal Reserve to declare a quadruple increase in a rate or, what is even worse, begin to sell assets from the balance that will turn back reduction of the liquidity in the system. Now the Federal Reserve reinvests the income from assets on balance so, in fact, there are injections of a money in a financial system.

The Yellen’s press conference was traditionally contradictory, overflowed with statements that increase in a rate isn't connected with revaluation of prospects of economy and changes in the course of monetary policy. It remains unclear what such positive occurred in the economy of the USA since December that FRS decided on an increase in a rate because the Atlanta FRB forecast for GDP growth of the USA in 1 quarter is at the level 0,9%, and inflation stood at 1,7%. Yellen thinks it’s not a time for reducing the FRS balance. It is clear – credit bubbles are so inflated that can burst in case of the slightest wrong move, and then nothing salvage from the next crisis. FOMC members expect two more increases in a base rate (to 1,375%), and it is logical to expect the growth of dollar in the near future against the background of strengthening of aggressive rhetoric. Contradictions on GDP growth of the USA between FRS and Trump's administration mean two possible scenarios:

- Trump's program will be accepted: then FRS will review the forecasts for the increase and dollar will grow. In this case, FRS opinion at the current stage can be ignored.

- Trump's program won’t be accepted in the nearest future: FRS shall correct the forecasts down, tax reform will be reduced for an indefinite time, and the stock market will look for a new bottom. FRS shall solve all of these problems.

The deadline for US national debt ceiling, about which Obama and Boehner agreed in October 2015, expired on 15th of March. At the moment this amount is refrigerated on a mark of $20 trillion. If to consider that the average inventory of the U.S. Treasury cash constitutes about $200 billion which is spent with a speed of $75 billion a month, then by summer America is waited by the next crisis, including the threat of a technical default and termination of work of the government. Naturally, nobody wants that the Treasury was at the end of the resources after which it should choose between payments on a debt and interest payments according to the last - to a point which will announce that the market has lost trust to the American debt. The bond market gives reaction already: profitability of bonds grows, and their prices down, even against the background of the rapid growth of the S&P/Dow/Nasdaq indexes. In today's America, a war of politicians reached such heat that the default can really take place.

The main result of the summit of G20 Ministries of Finance and heads of the Central Bank: lack of the accurate formulation about opposition to all forms of protectionism, and because of dogmatic refusal of the United States to accept a general opinion. The USA obviously prepares not only for trade wars, but also for currency. Trump's meeting with Merkel left a dual impression not only by the unwillingness of the American president to shake hands with the German leader.

Merkel didn't support Trump's suggestion to conclude the separate bilateral agreement with Germany (outside the EU) as it leads to the destruction of the euroblock and approval of the USA as main world consumer. It is worth paying attention to yuan exchange rate after the summit of G20 Ministries of Finance and heads of the Central Bank - further decrease against the dollar will confirm the lack of a consent between China and USA and then it is worth waiting for the beginning of an active trade war the next months.

The British parliament has ratified the bill about Brexit, May has confirmed the intention to initialize article 50 about an exit of Britain from the EU in the next 2 weeks. However, the EU isn't going to begin negotiations before payment of debts by Britain to the EU and the end of elections in Germany – Europe has optimum terms of negotiations with rebellious Britain today. EU diplomats who look for breaches in the English positions will carefully monitor political actions and May’s reaction to the current decisions.

The Bank of England at the regular meeting has declared that it continues to consider the current growth of inflation temporary, and the current policy - an adequate to the situation. The decision led to the growth of pound, as was expected by BoE. Of course, increase in rates in Brexit situation is impossible, but the galloping growth of inflation will put Britain in a difficult situation, the simplest way out – support of pound rate through more aggressive rhetoric.

In the nearest future, we can expect the raised pound volatility because the growth of inflation will lead to its growth, and delay of growth of economy against the background of expectation of Brexit − to sales. The current week the attention of market participants will be focused on the block of data on inflation on Tuesday and retail sales on Thursday. Fall of retail sales will be negative for pound, but if retail sales grow above the forecast against the background of inflation growth, then we can expect the growth GBP/USD higher than 1,25.

Market reaction to the decision at the American rate was excessive, the forthcoming week it is logical to expect to toughen of FOMC members rhetoric, Dudley’s performances on Tuesday and Yellen’s on Thursday can be the most aggressive. Quite suitable moment for Yellen to increase market expectations concerning the change of a rate in June. So far Trump doesn't manage to find consensus with the Congress in questions of reforms that is very negative for the dollar, but the president has a few months. Trump's performance on Monday will hardly be saturated by new information, but it is worth tracking.

The preliminary release of PMI of the industry and services on the Eurozone should be tracking, on the USA – balance of payments and statistics of housing. Ewald Nowotny's comments call into question statements of the ECB following the results of the last meeting: in his opinion, the deposit rate can be raised earlier, than the base crediting rate of banks. It is the most probable that the ECB will begin correction with deposits and only after bringing this rate to neutral value will start to increase the main rate.

The current week the ECB will hold working meetings (Wednesday-Thursday), information on opinions of participants can leak out into mass media, but this time the leakage can be intentional for leveling of expectations of the market about the nearest finishing of evroQE. EUR/USD on such background will surely fall. Draghi will insist on preserving the current policy before the results of the French elections, and fall of quotations of oil will help the head of the ECB.

On Monday evening 5 candidates for president of France, Marine Le Pen, Macron, Fillon, Amon and Melenchon will carry out television debates, and three from participants are in process of criminal investigation at the moment. If as a result, Marine Le Pen's rating grows, then euro practically have no chances of growth. The positive of Macron’s rating will be followed by growth of euro.

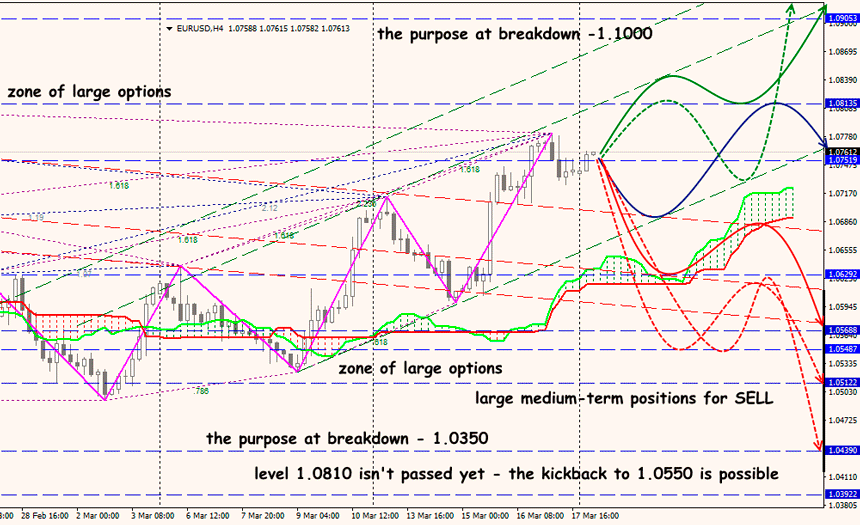

Technical Analysis EUR/USD

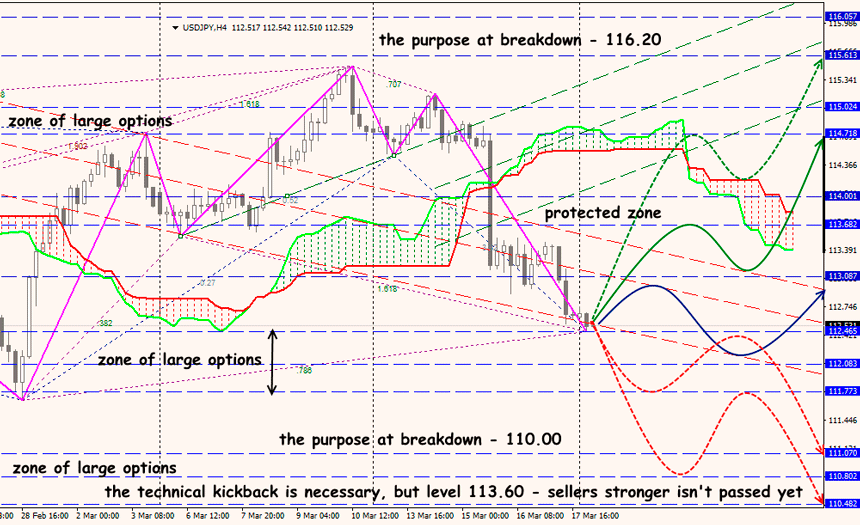

Technical Analysis USD/JPY