骚动而矛盾的时间

Last week neutralized all reasons for the growth of euro: the pound sturdily sustained Brexit start, Scotland prepares the second referendum, FRS saves optimism, Trump prepares for a trade war, Libya helped to oil price to grow.

ECB reported about saving the current policy by the authorized information leakage through affiliated media, that was confirmed afterward by data on EU inflation, while the American data are specified continuation of an economic recovery and inflation. Reuters agency, referring to sources in Board of governors of the European Central Bank, reported about an incorrect interpretation of rhetoric of the regulator following the results of a meeting on March 9. Measures of oversoft QE won't be contracted still the long time. EUR/USD oversold after achievement of important supports testifies, at least, in favor of deceleration of falling till obtaining new data.

Draghi is going to perform twice (Tuesday-Thursday) and can quite concentrate the attention of investors on the correctness that will lead to falling of profitableness of state treasury bills of Eurozone countries and euro exchange rate. But if Draghi doesn't begin to use such chance for manipulations, so there are serious fears of inflation growth in the future and neutral situation will remain at a meeting of the ECB on April 15. The publication of protocols on Thursday will hardly tell something new, but it is necessary to be afraid of leakage of info in media after the intermediate meeting of the European Central Bank on Wednesday.

Europe and Britain start to settle accounts. Today the pound − practically the cheapest currency of G10 based on the ratio of the current and fair value, but present pessimism on royal currency signals that bears frankly overcarry. May`s negotiations with Nikola Sturgeon didn't stop separatist moods in the United Kingdom.

The rigid option of negotiations on Brexit is negative for the British currency, but there is a hope for a pragmatism and the mutually advantageous agreement. If negotiations between Great Britain and EU are constructive, the sterling has the good potential for restoration. If negotiations aren't smooth, that is the risk that the course GBP/USD can fall to 1.1800, but if it and occurs, then such falling should be considered as an entry point in long-term long.

The European Commission has stopped the transaction on merge of two largest exchanges Deutsche Boerse (in Frankfurt am Main) and the London stock exchange (LSE) which even in the spring 2016th has agreed about merge by exchange of shares. It would lead to the emergence in Europe the exchange platform with capitalization more than $30 billion (the 3rd place after New York and Tokyo share). Against the background of Brexit London`s attempts to keep the all-European financial center cause at EU antimonopoly authorities fear about monopolization of clearing payments, especially according to transactions with debt securities. Now chances of the merge are minimum, but both exchanges can begin active work on customer capture from BRICS countries on primary placement and gradually increase capitalization.

After the initiative with replacement of Obamacare has failed in the Congress, Trump intends to sign the decree on carrying out a large-scale research of the reasons of trade deficiency in the USA, a bad collecting of anti-dumping duties and all other, called the president «abuses in trade» (dumping, illegal privileges, unilateral trade practicians of other countries and currency speculation). WTO rules which allow exempting export from the VAT, but at the same time don't exempt the American export from corporate income tax, are also subject to check.

Not casually preparation of such documents fell on very delicate period – current week the first meeting of Trump with the colleague Xi Jinping in Florida is planned, and questions of mutual trade will obviously be the principal stumbling block. If agreements aren't reached – it is necessary to expect the beginning of currency and trade wars, in the first stage, before the introduction of a boundary tax, these wars will be followed by falling of dollar exchange rate. In the 2016th the People's Republic of China made the biggest contribution to a deficit of trade in commodities in the States, (about $734 billion), further there are Japan ($69 billion), Germany ($65 billion), Mexico ($63 billion), Ireland ($36 billion) and Vietnam ($32 billion). The period for experts – 90 days.

Last week amicable injections of information from FRS convinced the markets that, at least, two increases in a rate still are coming us. The hawk spirit of the minutes of March 15 is expected, but it will hardly surprise investors. Performances of FRS members speak about the active discussion at last meeting the start date of balance reduction. At the moment QE works, but within fixed volume, and even hints for possible termination (or decrease) reinvestments will exert a much bigger impact on the markets, than the increase in rates. Taking into account intention of the US Congress to begin discussion of tax reform in the spring with ratification by August, it is logical to assume that FRS prepares the plan for decreasing of balance at a June meeting because, by that moment the forthcoming tax reform will take form, its volume, composition and periods of start will become clear. So the published protocols – we read attentively. Anyway, the influence of the protocol on the dollar will be short-term, the bravest can catch thorns on the publication according to the previous global trend.

Whenever possible, we recommend monitoring a situation in the US Congress which goes on Easter holiday on April 7. There is some chance of a compromise of Trump with democrats on improvement of the ObamaCare program and repeated vote, but even acceptance by the lower house «cancellation/replacement of ObamaCare» ratification by the Senate, most likely, will delay until the end of May that will lead to a delay of discussion of tax reform prior to the beginning of summer.

As regards traditional NFP on Friday: FRS is considered that US labor market has reached almost full employment, and therefore the number of jobs lower than the forecast won`t become a reason for revision of the main positions. Strong reaction is possible only when falling lower than 75K. The main attention – on the growth of salaries and unemployment rate (growth will become negative and will lead to the sharp decline of the dollar). The more exact idea of the quality of nonfarm will give ADP and ISM reports.

The regular meeting of the Eurogroup on April 7 will continue the immortal saga about the help to Greece. In the absence of the agreement on the second review of the aid program, Greece won't be able to pay debts to creditors in July that will bring to next technical default. It will be interesting to trace dynamics of ratings Macron/Le Pen by the result of televised debates on April 4 – euro has to react.

It is worth paying attention to the report of Tankan current week: depreciation of yen against the background of growth of the volume of world trade and strengthening of corporate inflationary expectations can seriously influence the BOJ strategy of monetary policy. On Monday and Tuesday, the Chinese markets are closed, their return on Wednesday can give volatility to Asian assets. Prior to EU leaders summit on April 29 the main attention of investors will be directed to economic data on the Eurozone and especially – the British statistics.

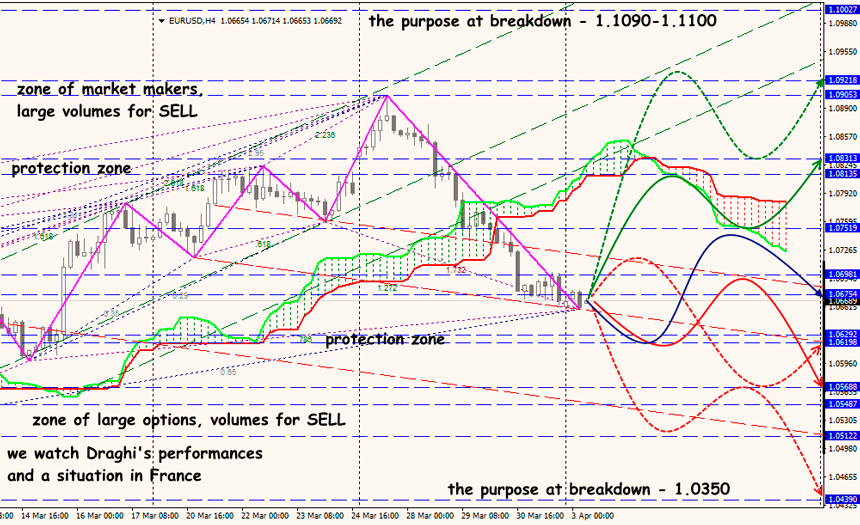

Technical Analysis EUR/USD

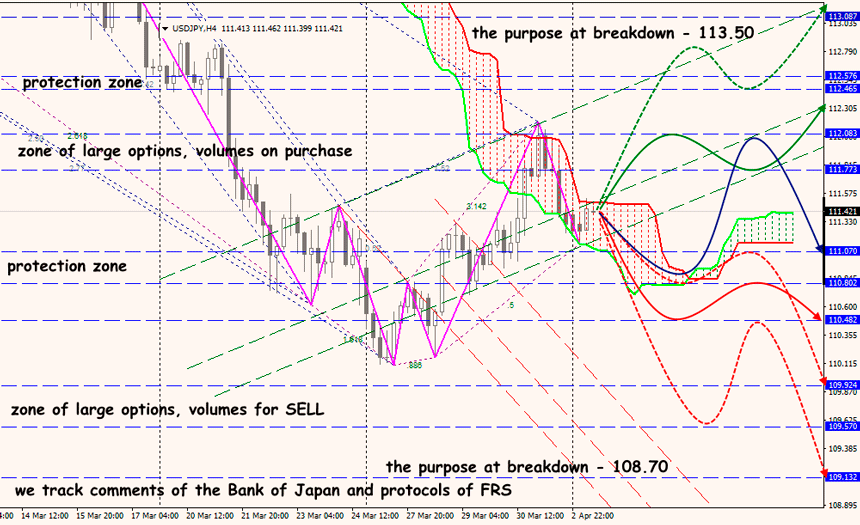

Technical Analysis USD/JPY