Federal Reserve vs. Trump: New Scenarios

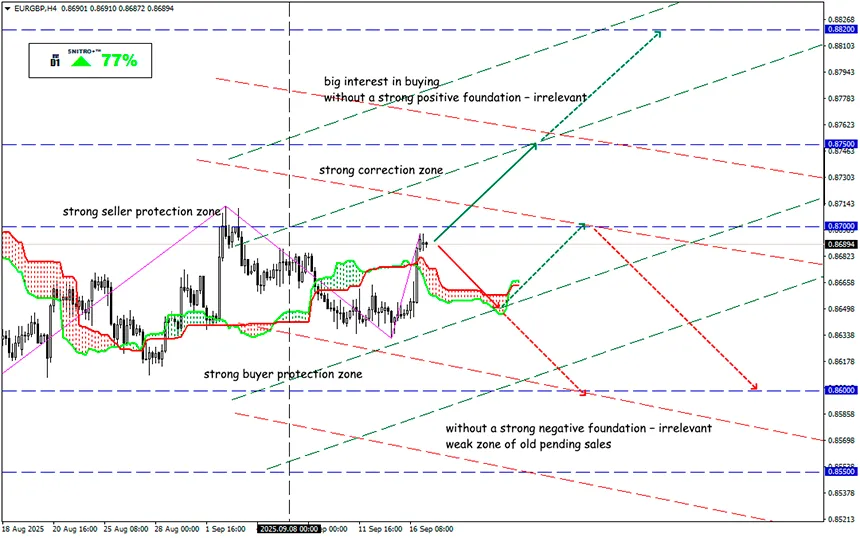

#EURGBP

Key zone: 0.8650 - 0.8700

Buy: 0.8700 (after a retest of 0.8650); target 0.8850; StopLoss 0.8640

Sell: 0.8600 (on strong negative fundamentals) ; target 0.8500-0.8450; StopLoss 0.8660

We are about to witness the strangest FOMC meeting of the past 10 years. The market logically expects a 0.25% rate cut following the collapse of the labor market, but the decision comes under direct political pressure from the Trump administration. This brings not only the real threat of losing Fed independence but also doubts about its effectiveness.

Politics vs. Finance

Trump’s personal aggression against the monetary regulator is further complicated by lawsuits, where until the last moment the list of participants was kept secret. As a result, Lisa Cook could not be removed from voting, but instead Trump quickly appointed his economic advisor to the vacant seat, with the clear goal of lobbying his own interests.

The main intrigue: two or three cuts

A 0.25% cut is already seen as inevitable, so investors are focused on the Fed’s forward guidance. The key question is how many cuts will appear in the quarterly forecast. This will set the tone for the two remaining FOMC meetings this year and will dominate Powell’s press conference.

Labor market vs. inflation

The Fed’s forecasts must answer three questions:

- How dangerous is the slowdown in the labor market?

- How fast should rates be cut to reach the “neutral” level?

- Where is this “neutral” level right now?

The answers remain unclear. Employment data looks catastrophic: in July, the average monthly job gain was 150,000, after revisions it was 96,000, and over the last three months only 29,000. For the first time since 2021, the number of unemployed has exceeded job openings.

In July, the Fed left rates unchanged, citing inflation risks, though Powell hinted that the balance of risks pointed to a neutral rate. In his view, this is 4.3%, while other officials see it at 3%. The macro backdrop today is less favorable for aggressive easing than a year ago.

What matters now is Powell’s tone: last month he already expressed more concern about the labor market than inflation. The question is whether he will strengthen this message after the weak August report.

Across all major assets, key levels have accumulated deferred volumes that will be speculatively traded on the Fed’s announcements, while yen pairs will also react to BOJ updates. This could generate technical reversal signals in medium-term trends, but such signals will only hold if supported by fundamentals.

So we act wisely and avoid unnecessary risks.

Profits to y’all!