Stocks & Gold: One Trend for Two

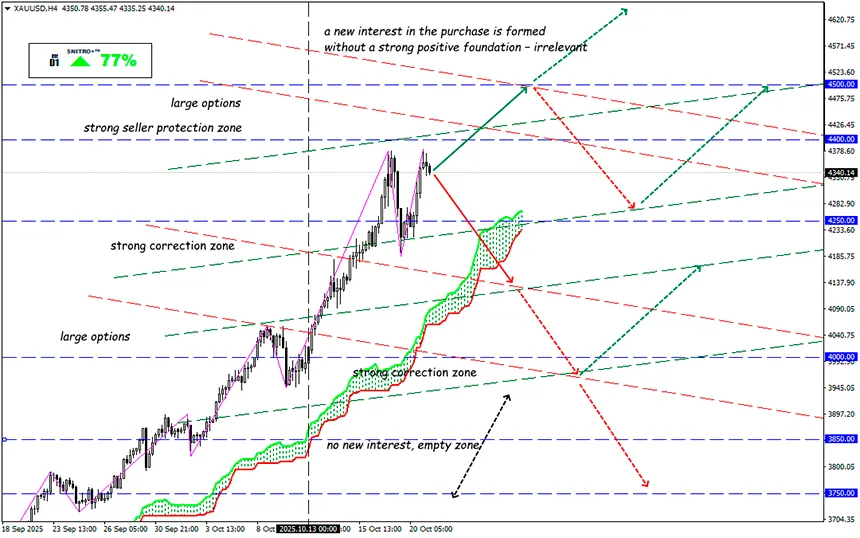

XAU/USD

Key zone: 4,250.00 - 4,350.00

Buy: 4,400.00 (on a strong positive foundation); target 4,600-4,650; StopLoss 4,320.00

Sell: 4,250.00 (on a strong breakdown of the 4,300 level); target 4,000.00; StopLoss 4,320.00

There are many anomalies in the modern market, but one of them causes panic among beginners and nervous tics among experienced players. Gold is behaving as it did during the wild inflation of the 1980s, while the stock market seems stuck in the euphoria of the dot-com era. Classical fundamental analysis claims that gold (and all precious metals) cannot—or should not—rise simultaneously with stocks. Previously, the correlation between gold and stock prices was zero, but this pattern no longer works.

Remember: the money that entered the market never leaves it; it only redistributes within the market process.

The trillions of dollars pumped into the economy by governments during and after the COVID-19 pandemic still “feed” activity across all markets—from equities to gold.

Some believe that gold prices are rising because investors want to hedge against growing political uncertainty—especially during periods of wars and erratic politicians.

But why then are investors showing such ungrounded optimism toward American AI stocks while ignoring the risks associated with dollar volatility? Today, there are more reliable ways to hedge risk than gold—for example, buying PUT options on stocks, which is simpler and cheaper.

The real reason for this anomaly is excess liquidity. The volume of U.S. funds held in money market mutual funds has reached $7.5 trillion—$1.5 trillion above the long-term trend.

Liquidity growth is fueled by investors’ risk appetite: the higher the confidence in asset growth, the more capital flows into the market. U.S. households are increasing stock trading volumes, expecting government support at the first sign of trouble. Innovative trading apps with low commissions make asset buying instant and widespread.

The result is a sharp drop in the risk premium, guaranteeing an uncontrolled liquidity influx.

Gold’s rally intensified after 2022, when the dollar became a sanctions tool and central banks began actively buying gold as an alternative reserve asset. However, activity has now shifted toward ETFs: capital inflows have grown ninefold, and their share in total gold demand has reached almost 20%.

The argument about fear of dollar depreciation is no longer valid—the dollar has been stable in recent months, yet gold keeps breaking records. Bond market indicators also fail to explain the move: yields match inflation expectations around 2.5%.

Meanwhile, other non-hedging assets are also rising—silver, platinum, leveraged ETFs, unprofitable tech firms, and junk bonds with poor management quality.

All of this will eventually fall in sync as well.

If consumer inflation accelerates again and the Fed is forced to tighten policy, investors may face an unpleasant surprise: gold could fall along with AI stocks, destroying the old perception of market “insurance.”

So we act wisely and avoid unnecessary risks.

Profits to y’all!